adidas Publishes Fiscal Q1’23 Financial Report

- Currency-neutral revenues flat versus the prior year despite adverse Yeezy impact

- Gross margin down 5.1pp to 44.8% due to higher supply chain costs, increased

discounting, inventory allowances, adverse Yeezy impact and negative FX movements - Operating profit reaches €60 million

- Inventory position improves sequentially to €5.7 billion, up 25% versus the prior year

- Full year outlook confirmed

adidas CEO Bjørn Gulden commented:

“Q1 ended a little better than we had expected with flattish sales and a small operating profit

of €60 million. Sales growth excluding Yeezy was 9%. Great double-digit growth in Latin

America and Asia-Pacific, and slight growth in EMEA despite Russia were in line with our plan.

Total revenues in Greater China were still down 9%, but we achieved double-digit sell-out

growth. This was better than expected and makes us optimistic for the rest of the year. The

20% sales decline in North America – down 5% excluding Yeezy – was in line with our

conservative sell-in strategy due to the high levels of inventory and discounts in the market.

We are very happy to see our Performance categories continue to develop well and grow

strongly. The decline in Lifestyle and the loss of Yeezy are of course hurting us. But also here

we see some positive developments: The Terrace segment is doing very well in all markets

and we have started to scale up volumes for our Samba, Gazelle and Campus franchises. Our

partnership launches with Bad Bunny, Ronnie Fieg/Kith and Gucci have performed great. And

the reaction from consumers and retailers to our Fear of God launch in April was incredible.

Inventories are still too high, but already €300 million lower than at the beginning of the year.

We continue to work hard to normalize our inventory levels during the year. This is crucial for

us to be able to lower discount levels, increase our full price business and re-build brand heat

again.

I have spent Q1 working on our product ranges, brainstormed about future innovations, talked

to a great number of retailers about improving our cooperations, met suppliers to discuss

future strategies, had many of our athletes visiting our campus, and of course started to work

on simplifying and speeding up our processes. All of this will continue, and we still have a long way to go, but I am very happy with the progress we have made and what we have achieved so

far.

I am extremely inspired by the huge energy and talent our people – the adidas family – have

showcased during the short time I have been here. adidas has all the ingredients to be the

best sports brand in the world, to grow strongly and to be a good profitable company. We just

need some time. 2023 will be a bumpy year with disappointing numbers, where maximizing

our short-term financial results is not our goal. It is a transition year to build a strong base

for a better 2024 and a good 2025 and beyond.”

Currency-neutral revenues reach prior-year level

In the first quarter of 2023, currency-neutral revenues were flat versus the prior-year level.

The top-line development in Q1 was impacted by significantly reduced sell-in to the wholesale

channel as part of the company’s initiatives to reduce high inventory levels, particularly in

North America and Greater China.

The discontinuation of Yeezy produced a €400 million drag. Footwear revenues grew 1% during the quarter, reflecting the strong momentum the adidas brand is enjoying in its Performance categories football, running, outdoor and tennis. Apparel sales declined 3% in the first quarter as this product division is particularly impacted by the high inventory levels in the marketplace and the company’s disciplined sell-in approach in response to it. Accessories grew 8% during the quarter driven by strong growth in football.

Lifestyle – including sunglasses – revenues were down during the quarter despite extraordinary demand for the company’s Samba, Gazelle and Campus franchises. These products are at the core of the current Terrace sneaker trend and have been benefiting strongly from it. While adidas continued to limit the supply at the beginning of the year, the company is slowly starting to scale its offering as the year progresses.

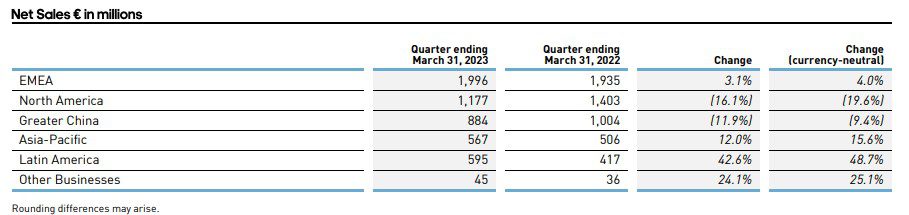

Wholesale revenues grow strongly in EMEA, Asia-Pacific and Latin America

From a channel perspective, currency-neutral sales in Wholesale grew 3% driven by strong

growth in EMEA, Asia-Pacific and Latin America. Direct-to-consumer (DTC) revenues

declined 7% versus the prior year. This development reflects the adverse Yeezy impact on the

company’s e-commerce business (-23%) as the vast majority of this product used to be sold

through adidas’ own online channel. At the same time, sales in the company’s own retail

stores increased 11% in Q1.

Gross margin declines to 44.8%

adidas‘ first quarter gross margin was down 5.1 percentage points to 44.8% (2022:

49.9%). This decrease was mainly driven by the increase in supply chain costs as well as

higher discounting in the marketplace. In addition, inventory allowances, the adverse Yeezy

impact and negative currency developments weighed on the gross margin development. This

could not be offset by the significant positive effect from the price increases the company has

implemented.

Net loss from continuing operations of €24 million

After taxes, the company’s net loss from continuing operations amounted to €24 million

(2022: net income from continuing operations of €310 million), while basic EPS from

continuing operations decreased to negative €0.18 (2022: positive €1.60).

adidas confirms full year guidance

For the full year 2023, adidas continues to expect currency-neutral revenues to decline at a

high-single-digit rate as macroeconomic challenges and geopolitical tensions persist.

Elevated recession risks in North America and Europe as well as uncertainty around the

recovery in Greater China continue to exist. The company’s revenue development will also be

impacted by the initiatives to significantly reduce high inventory levels. In addition, while the

company continues to review future options for the utilization of its Yeezy inventory, the

guidance reflects the revenue loss of around €1.2 billion from potentially not selling the

existing stock. Accounting for the corresponding negative operating profit impact of around

€500 million, the company’s underlying operating profit is projected to be around the breakeven level in 2023.