Revenue Growth Delivers Strong Group Performance for Globe’s H1 FY26

H1 FY26 Financial Highlights

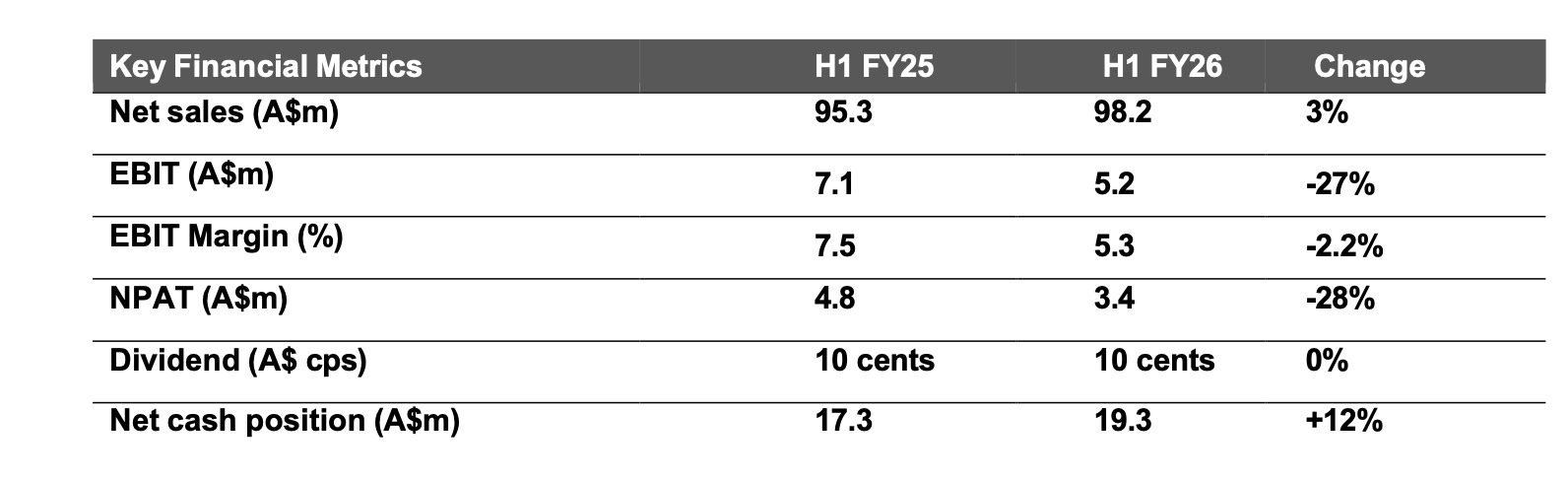

Revenue of $98.2 million (H1 FY25: $95.3m)

EBIT of $5.2 million (H1 FY25: $7.1m)

NPAT of $3.4 million (H1 FY25: $4.8m

- Return to revenue growth across the Group (+3% vs. prior corresponding period (PCP)) despite challenging trading conditions.

- Continued focus and solid performance from global brands which present long term scale and growth potential (FXD, Salty Crew and Globe).

- Strong gross margin management, however, US gross margin temporarily impacted by tariffs, with improvements expected in H2.

- Australian improved business mix resulting in higher margins and profitability growth.

- US revenue growth of 3% vs. PCP on like for like brand basis, amid challenging market conditions and temporary margin impact of tariffs. Expectation of improvement in revenue and profitability in H2.

- Strong European sales performance with growth of 21% vs. PCP, benefiting from an operational reset.

- Fully franked interim dividend of $0.10 per ordinary share (cps) declared (H1 FY25: $0.10 cps).

- Solid cash flow and financial position with a strong balance sheet and net cash of $19.3 million.

- Foundations now in place for growth – expectation of revenue and profit increase in H2 with the full year expected to be ahead of FY25.

Commenting on the H1 FY26 results, Globe International CEO, Matt Hill said:

“The Group produced a solid result with revenue and profit in line with expectations, with the consolidated entity achieving 3% total revenue growth to $98.2 from $95.3 million compared with the PCP.

In the first half of the year the Group delivered EBIT of $5.2 million, which represents a 5.3% margin. While $1.9 million down on the PCP, the result was impacted by the short notice of introduction of increased tariffs in the USA that affected the first half of the financial year in the region. Swift action was taken to absorb this new operating environment into the financial planning of the business in the USA and as such, at the current levels, tariffs are not expected to impact performance in the same way going forward.

For the period, core brands of Salty Crew, FXD and Globe contributed strongly to Group revenue and profit. Salty Crew grew in the half, with the brand growing well in traditional doors, new product categories and the broader outdoor market. FXD continued to be a powerhouse in its workwear market and a large contributor to company revenue and profit while Globe brand grew in all regions.

Having now dealt with the brunt of the short-term challenges of tariffs in the first half, the Group emerges with improved margins in core brands and a stronger platform from which to deliver sales growth and improved profitability into the future”.

As at 31 December 2025, the Group’s cash position, net of working capital borrowings, was $19.3 million, which was consistent with the net cash position at the end of the 2025 financial year. Cash generated from operations was $7.4 million, driven by a $3.3 million reduction in working capital associated with a decrease in trade receivables during the period offset by traditional seasonal inventory build at the half year. Cash utilisation during the half year was driven by non-operating factors including dividends and capital expenditure.

Taking into consideration the Group’s earnings performance, strong balance sheet, and outlook for the business, the Board has declared a fully franked interim dividend of $0.10 (cps) (H1 FY25: $0.10 cps). The interim dividend will be paid to shareholders on 27 March 2026.

Commenting on the outlook for Globe, Mr Hill said:

“Globe continues to deliver upon its strategic objectives of focusing increasingly on higher sales and margin growth in its global brands. The Group held up extremely well financially in the first half of the financial year, delivering growth, returns to shareholders, and dealing with the broader economic challenges presented during the trade period. Following this period, Globe emerges with a strong balance sheet, performing brands and improved margins which is anticipated to drive revenue and profit growth in 2026.”