Pro Content

Pro Content

JD Sports Interim Results 2025/26 Continued focus on operating & financial discipline

“We delivered organic sales growth of +2.7% in H1, in what remains a tough trading environment. This demonstrates the resilience of our business, underpinned by our agile multi-brand model, broad geographic reach and unmatched connection with customers, commented CEO Regis Schultz.

“In North America, where we gained market share in the period, the development of our operations is progressing well. We continue to build strong brand awareness of the JD fascia by building out our customer proposition and investing in new stores; and for our complementary fascias we are successfully progressing the integration of Hibbett, while DTLR and Shoe Palace took over the operations of City Gear in June.

“Our supply chain investments are poised to unlock significant efficiencies across our global network. Our new European distribution centre in Heerlen, the Netherlands, is set to launch automation for JD Europe store replenishment in the coming weeks, while our US west coast site in Morgan Hill is set to go live with JD and Finish Line by year-end – the next step of our plan to leverage our distribution centres on a multi-fascia basis.

“In an environment of strained consumer finances and evolving brand product cycles, operating and financial discipline remains a core focus for JD, and we are controlling our costs and cash well. Whilst we remain cautious on the trading environment for the second half, we expect limited impact from US tariffs this financial year, and our full year profit before tax and adjusting items to be in line with current market expectations.”

H126 HEADLINES:

Market share gains(1) in key growth markets of North America and Europe, against tough consumer backdrop

Strong progress against strategic objectives across omnichannel customer proposition, store footprint, supply chain and North America operations. Costs and cash being well controlled

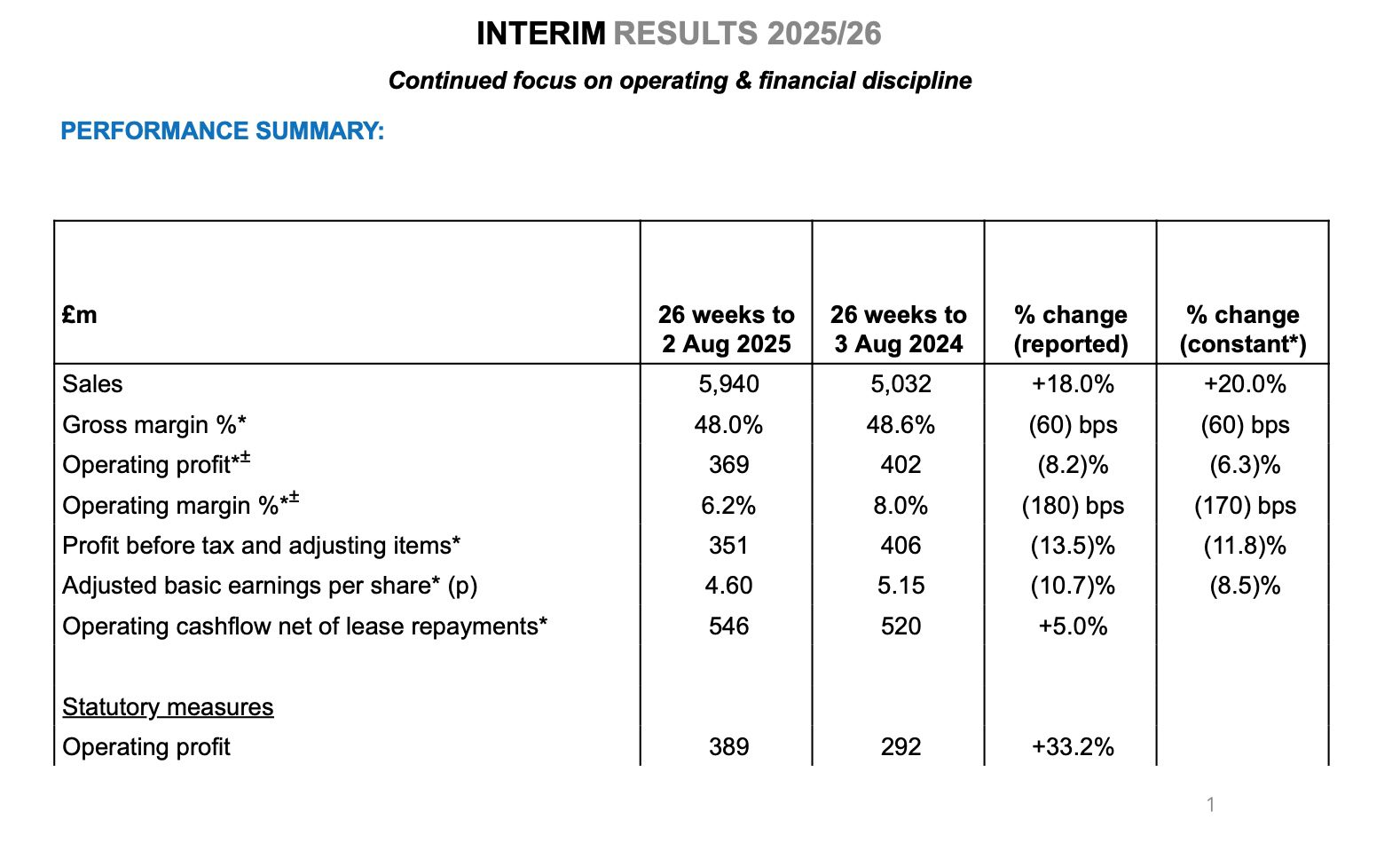

Total sales +20.0% (at constant FX rates) driven by acquisitions of Hibbett and Courir; organic* sales +2.7% (at constant FX rates) and like-for-like* (LFL) sales -2.5%

Stronger LFL sales trends in apparel and online in North America; resilient LFL sales in Europe, and UK organic sales(2) affected by tough Q2 comparatives due to Euro 2024 football tournament

Good underlying performance in apparel globally; footwear softer given ongoing shift in product cycle

Gross margin of 48.0%, 60bps lower YoY (40bps lower YoY excluding Hibbett and Courir). Maintaining trading disciplines with controlled price investments, particularly in online

Profit before tax and adjusting items (PBTAI) of £351m, in line with guidance given on 27 August

Expect FY26 PBTAI to be in line with current market expectations(3,4), with limited impact expected from US tariffs this financial year

CHIEF EXECUTIVE OFFICER’S REVIEW

JD Sports is reinforcing its position as a leading international sports fashion powerhouse, in an attractive and growing market which benefits from ongoing casualisation and active lifestyle trends. In a tough trading environment in the short term – in terms of strained consumer finances together with evolving brand product cycles in athleisure – we have remained calm and focused on consistent execution against our strategic priorities, and strict operational and financial discipline. This is evidenced by market share gains in our key growth markets of North America and Europe in the period.

Above all else, we remain obsessed with delighting our customers by evolving our multi-brand product assortment – including the latest and exclusive premium sports fashion, expanding and enhancing our store footprint, strengthening our omnichannel capabilities, and improving the efficiency of our supply chain to ensure strong product availability and fast fulfilment.

While we recognise that consumer behaviours are evolving in the face of broader uncertainty across the world, by staying close to our customers and brand partners, we believe we can continue to lead with the right products, at the right time, in the right place. Our strong and agile multi-brand business model, underpinned by disciplined execution and a clear strategic focus, positions us well to navigate these challenges.

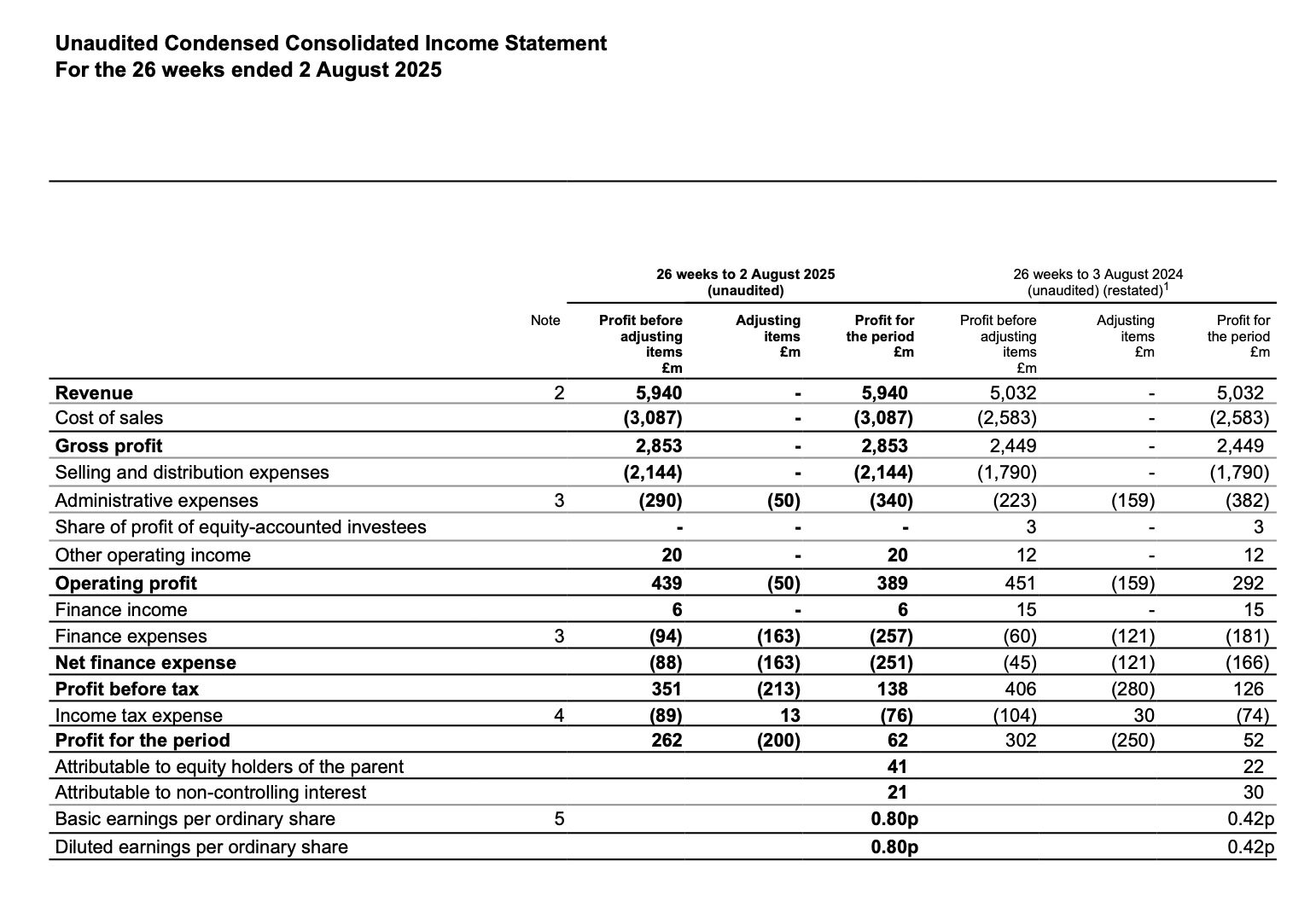

Turning to our performance in the 26 weeks to 2 August 2025, we achieved sales of £5,940m, +18.0% on the comparative period, or +20.0% at constant FX rates. Excluding the two businesses acquired in FY25 (Hibbett and Courir), organic sales growth was +2.7% at constant FX rates, which includes a +5.2%pts benefit to sales from net new stores opened across the Group. We believe +2.7% is faster than the growth of our addressable markets, driven by market share gains in North America and Europe. Group LFL sales were -2.5%.

Excluding Hibbett and Courir, the gross margin % for the Group in H1 was 40bps lower YoY. This was largely driven by controlled price investments in the online offer to boost competitivity and increase engagement with online customers. Including acquisitions, the overall Group gross margin % in H1 was 60bps lower YoY at 48.0% (H125: 48.6%).

We are a highly cash generative business, with £546m of operating cash flow (after lease repayments) in H1 +5.0% YoY. Given the seasonality of our business, it is normal to see working capital outflows in the middle of the financial year, before normalising around the year-end. At the end of H1, we had net debt (before lease liabilities) on our balance sheet of £125m. We expect to move to a net cash position (before lease liabilities) by the year-end

Regional commentary

North America is our largest market by sales, generating 39% of JD Group sales in H1, with Europe at 32%, the UK at 25% and Asia Pacific at 4%.

LFL sales in H1 were resilient in Europe, supported by our sporting goods fascias in Iberia, Greece and Cyprus, and it was encouraging to see improved LFL trends quarter on quarter in both North America and Asia Pacific. In H1, we grew our market share in North America and Europe (source: Circana). In the UK, we see organic sales as a better sales KPI than LFL, given the ongoing evolution of our store footprint with ‘bigger and better’ stores. See footnote 2 on page 2 for further details. UK organic sales were -1.7% in H1, affected by tough prior year

JD UK

The UK is JD’s most mature market and saw revenues fall 1.8% to £1,214m. Net new space growth was 1.7% alongside a 2.9% reduction in LFL.

The first quarter saw dry, warm weather which drove conversion in stores enabling us to uphold our pricing disciplines. The second quarter had challenging comparatives from the prior year Euro 24 football tournament alongside strong franchise footwear trends, particularly in womens and juniors.

Performance in apparel has been robust, driven by a strong and compelling proposition, especially in womens and juniors. Footwear has seen a transition in trend from ‘end of cycle’ key product lines into newer franchises. Operating profit before adjusting items and after lease interest* was down 6.2% driven by an increase in people costs due to wage legislation, increased property costs from annualised stores and new store openings, including the Trafford Centre, Manchester and investment in technology infrastructure and cyber resilience.

JD Gyms revenue increased 10% to £67m as the number of operating gyms increased from 92 to 97, following the acquisition of three gyms and the opening of two in the period.

JD Europe

JD Europe growth continues to be driven by new store rollouts and conversions supported by a maturing estate and increasing market awareness of the JD brand. Revenue grew 12% to £1,094m and by 12% on a constant currency basis. Organic sales growth was 12% , comprising net new space growth of 12.8% and a 0.8% reduction in LFL sales*.

Extreme weather events have impacted store footfall over the period, however online traffic and conversion has continued in a positive trend with the ongoing roll out of ship from store and click-and-collect supported by targeted promotional activity. The second quarter had challenging comparatives from strong franchise footwear trends, particularly in womens and juniors. While replica sales declined on the back of the Euro 24 football tournament, the impact was modest compared to the UK. Underlying apparel performance was driven by strong results in Northern markets, particularly in mens and junior categories