Pro Content

Pro Content

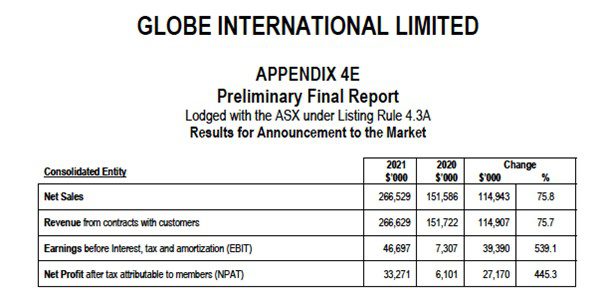

Globe International Limited Results for the Financial Year Ended 30 June 2021

The Group reported extraordinary growth in both sales and profitability as it benefited from having strong brands in industries and activities that consumers were able to participate in throughout the COVID-19 pandemic.

The key business metrics for the full financial year were as follows:

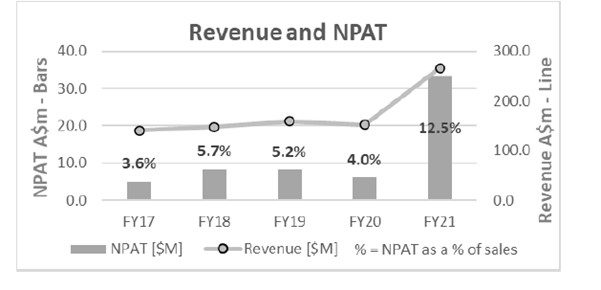

- Reported net sales for the financial year of $266.5 million were 76% higher than the prior comparative period

- Earnings before interest and tax (EBIT) were $46.7 million, more than 5 times the $7.3 million reported in the pcp.

- Net profit after tax (NPAT) of $33.3 million for the financial year was $27.2 million higher than the $6.1 million reported in the pcp.

- Cash-flows generated from operations were $22.5 million, as cash was invested in working capital to support the growth in revenues over the year.

Matt Hill said, “It was an exceptional year in so many ways. We delivered a record performance for the financial year as our business benefited from having a captive market for our products. Our consumers had government stimulus money to spend, but limitations on how to spend it due to the restrictions in place globally for much of the year. When our retail customers had to close their doors, we were able to capture those sales through our direct to consumer online platform, which experienced rapid growth at high margins. Then, as restrictions eased, we saw a strong rebound in wholesale sales. While we recognise that these tailwinds have contributed to the exceptional performance for the year, none of this would have been possible had it not been for our brands with their competitive position in each of their respective markets, our diverse business model, and the tenacity and commitment shown by our tight worldwide teams in such arduous conditions.”

The 76% growth in net sales was driven by the Group’s four main brand pillars of FXD, Impala, Salty Crew and Globe hardgoods. Together, these brands comprise all the Group’s core product categories of skateboards, apparel, footwear, workwear and roller skates. Regionally, all divisions reported sales growth of 50% or more. North America was the stand-out, delivering a 141% increase in revenues in local currency, partially fuelled by a shift towards online sales. Across the Group, in constant currency terms, online sales were four times higher than the corresponding period and wholesale sales grew by 63% for the year.

The $46.7 million of EBIT reported for the year represented 17.5% of net sales, compared to just $7.3 million and 4.8% of net sales in the prior financial year. The significant growth in earnings was driven by the growth in sales and the increase in gross profit margins. On top of this, overall costs grew at less than half the rate of sales growth, contributing to the significant increase in profitability. Overall costs for the financial year were somewhat suppressed due to spend limitations caused by COVID-19 restrictions, Government stimulus and, more generally, the time it took to add resources to keep up with the fast-paced growth in demand.

Matt Hill noted that “This was one of the toughest years we have had from an operational perspective. We have had to continually review and update our work practices to address the evolving risks posed by the ongoing COVID-19 pandemic, as the health and wellbeing of our global team continues to be one of our highest priorities. On top of this, we knew the demand was there for our products, our struggle was how to keep up with it. We had to adapt our systems to cope with the surge in demand. This included expanding our sourcing capacity, rapidly adapting our warehousing and distribution arrangements, and finding the right people to add to our global team. It’s something that we continue to invest in as we find the right balance for the current scale of the business.”

The Group’s net cash position at 30 June 2021 was $36.1 million, which was $10.1 million higher than the same time last year. Cash flows from operations were fairly consistent with the prior year at $22.5 million, as the Group invested in working capital to fund the continued growth in sales. Overall working capital levels are healthy and remain on the lower side of normal with respect to receivables days sales outstanding and months of inventory on hand.

Looking ahead, Matt Hill said. “We do not expect to see the kind of extraordinary growth in sales and profitability that was experienced during FY21, but we are optimistic about the position of our brands and their prospects this coming financial year. Trading conditions so far this financial year have been challenging but performance has remained solid.

However, the global effects of the evolving COVID-19 pandemic are having an impact on our business. The latest lockdowns across Australia, the strain on global logistics caused by container shortages and port congestion and closures, along with the global surge in new COVID-19 cases all create uncertainty. As such, we are currently not able to provide an outlook. We will have further information at our AGM in October, once the first quarter is behind us and we have more visibility into the second half of the financial year.

However, the global effects of the evolving COVID-19 pandemic are having an impact on our business. The latest lockdowns across Australia, the strain on global logistics caused by container shortages and port congestion and closures, along with the global surge in new COVID-19 cases all create uncertainty. As such, we are currently not able to provide an outlook. We will have further information at our AGM in October, once the first quarter is behind us and we have more visibility into the second half of the financial year.