Kathmandu Holdings Report Rip Curl Sales Up 2.7% in 1st Half of 2022

Strategic initiatives position KMD Brands for return to global growth, as reported in their half year financial statement for the period ending January 31, 2022.

1H FY22 key highlights (vs 1H FY21):

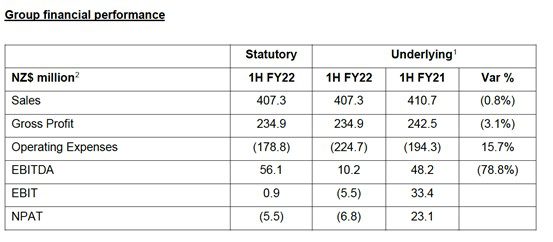

- Sales of $407.3 million (1H FY21: $410.7 million) positive Q2 rebound following Q1 COVID lockdown impacts on Kathmandu and Rip Curl in Australasia

- Oboz impacted by COVID closure of Vietnam factories (now reopened)

- Gross margin of 57.7% (1H FY21: 59.0%), due to elevated international freight costs, and increased clearance mix for the Kathmandu brand

- Underlying EBITDA of $10.2 million (1H FY21: $48.2 million)

- Statutory NPAT loss of $(5.5) million

- Strong balance sheet with $48.6 million net debt and comfortably within all covenants; significant funding headroom of c.$250 million

Commenting on the 1H FY22 results, Group CEO & Managing Director Michael Daly said:

“We continued to deliver on our strategic objectives, positioning KMD Brands for growth as travel rebounds globally and COVID-related impacts on supply abate. We maintained a strong focus on building our global brands, sponsoring the first ever World Surf League finals with the men’s event won by a Rip Curl surfer. We opened twelve new owned / licensed retail stores globally, and online sales increased to 17.4% of direct-to-consumer sales, rewarding initiatives to elevate digital capabilities. Substantial progress was also achieved on our ESG strategy

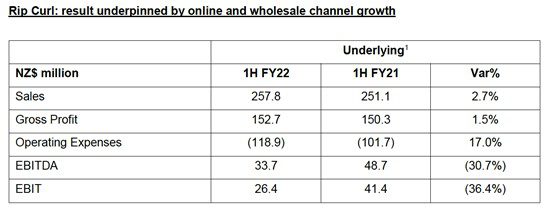

Rip Curl delivered sales growth of 2.7% over the half, with strong sales growth in online and wholesale channels, underpinned by strong performance in Europe and Hawaii in particular, while North America was impacted by short-term wetsuit shortages and port congestion. Rip Curl returned to same store sales growth in Q2, as lockdown restrictions lifted and the business rebounded

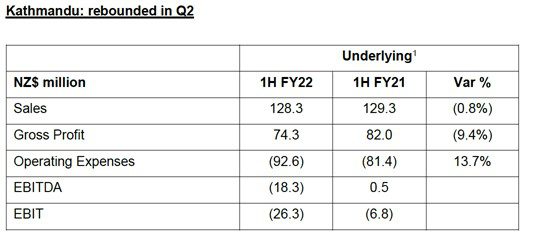

The Kathmandu Australasian store network was more impacted by COVID closures in Q1 than the Rip Curl global store network, before recovering strongly in Q2. While Kathmandu continued to feel the impacts of COVID related travel restrictions, we were pleased to see a 46.4% increase in online sales, and the business is well positioned to grow internationally, with the Europe Fall / Winter 22 sell-in complete, and forward orders in line with expectations

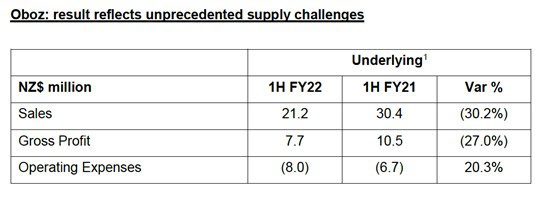

Oboz was impacted by the closure of Vietnam supplier factories due to COVID lockdowns, with approximately half of 1H FY22 orders unable to be fulfilled. However, the demand for the Oboz brand and products has never been stronger, with forward orders into FY23 very strong and supporting our medium-term growth targets

The 1H FY22 Group results were underpinned by positive Q2 sales following Q1 COVID lockdown impacts on Kathmandu and Rip Curl in Australasia. While these lockdowns impacted EBITDA by c. $35 million, Q2 underlying EBITDA was above last year reflecting the rebound in sales. The Group invested in the long-term value of all three brands, with an additional $14 million expenditure in 1H FY22 to support brand marketing.

Rip Curl’s results were supported by strong sales growth in online and wholesale channels, with total sales up 2.7% on 1H FY21. Europe and Hawaii in particular achieved strong sales growth, while North America was impacted by wetsuit shortages and port congestion, and Australia was impacted by COVID-related store closures during Q1. Direct-to-consumer same store sales growth (comprising owned retail stores and online) was up 2.1%, adjusted for COVID lockdowns3. Q2 same store sales growth was +3.0%, with +20.1% same store sales growth compared to Q2 FY20 (pre-COVID). Online sales grew by 14.5%, with penetration increasing from 11.5% of DTC sales in 1H FY21 to 13.8% of DTC sales in 1H FY22. Wholesale sales were up 16.1%, with less COVID interruption to the 1H FY22 sell-in period than last year. The slight reduction in gross margin to 59.2% (1H FY21: 59.9%) was due to a higher wholesale mix and elevated international freight costs.

Kathmandu’s performance continued to be impacted by COVID-related lockdowns and travel restrictions. Same store sales (including online) were up 3.0% overall, as a result of a strong Q2 rebound, where same store sales grew by +15.4%. Online sales grew 46.4%, with penetration increasing from 14.4% of sales in 1H FY21 to 21.2% in 1H FY22. Gross margin was impacted by an elevated clearance mix and elevated international freight costs.

Oboz wholesale and online sales were heavily impacted by the three-month COVID-related closure of Vietnam factories and compounded by international freight delays, with approximately 50% of 1H FY22 orders unable to be fulfilled. Oboz Vietnam factories have since reopened and are ramping up production, with supply expected to recover during 2H FY22. Gross margin was impacted by significant international freight costs averaging more than 300% over the historical average.

Strong balance sheet

The strong balance sheet position allows the Group to support growth investments and pursue attractive M&A opportunities. The Group had a net debt position of $48.6 million, with significant funding headroom of $250 million, with all debt facility covenants comfortably complied with. Inventory is $20 million above January 2021, and is being managed to mitigate increased production lead times and international shipping delays. January stock balances traditionally include stock build for key Rip Curl Northern Hemisphere summer and Kathmandu winter seasons. The adjusted operating cash outflow was $50.1 million.

Review of Operations

COVID-19 continues to cause ongoing disruption to our customers, employees, and suppliers globally. The disruption has resulted in reduced retail footfall, temporary store closures, supply chain delays and staffing constraints in many locations. As a result of these disruptions the Group has recorded a consolidated net loss after tax for the period of NZ$5.5 million (2021: NZ$22.3 million profit).

Significant store closures in Victoria, New South Wales, ACT and New Zealand heavily impacted Q1 sales and profitability with underlying EBITDA down c. $35 million on the prior period. Pleasingly Q2 rebounded strongly in Australasia as Kathmandu and Rip Curl grew on the comparable period. Oboz was materially impacted during the period as Vietnam factory shutdowns constrained supply and its ability to fulfil demand. Gross margin for the period was 130 basis points lower than last year due to elevated international freight costs, and increased clearance mix for the Kathmandu brand.

Operating expenses were carefully controlled during store closures and the Group continued to invest in the long-term value of all three brands, with an additional $14 million of expenditure in period to support brand marketing. Operating expenses reflect $15.2 million lower net government wage assistance and rent abatements than last half year.

Outlook

While we continue to navigate impacts from COVID on global supply chains, forward demand for our Rip Curl and Oboz products remains at record levels, and Kathmandu enters the traditionally strong winter season well prepared. We will continue to invest in building our global brands in the second half, with the launch of Kathmandu online sites in Europe and Canada and the merging of Canada and UK fulfilment centres for all brands. We remain focused on several key initiatives to elevate our digital capabilities, with the Club Rip Curl loyalty scheme due to launch in the second half.

Read the full statement on the KMD site here.