Pro Content

Pro Content

VF Corp Sees Gains In China, Europe Outperforming Americas

VF Corp just released their Q2 results. With half of the year done, and recent structural changes announced, where does the company stand?

Let’s have a look at the numbers, focusing on its two iconic action sports brands, Vans and The North Face.

Until this quarter, VF had its brands organised into three segments:

- Outdoor: The North Face, Timberland, Icebreaker, Smartwool, Altra.

- Active: Vans, Kipling, Napapijri, Eastpak, JanSport, Eagle Creek.

- Work: Dickies, Timberline Pro.

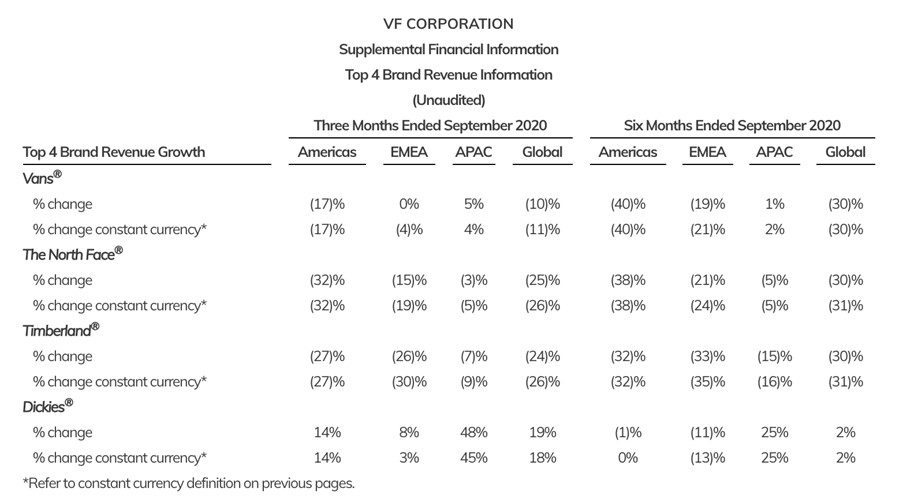

Its top four brand being Vans, The North Face, Timberland and Dickies. VF does not disclose revenue numbers by brand.

On October 13, VFC announced a new “Management Structure Around Core and Emerging Brands Portfolio”, re-shuffling the brands into two segments:

- Core: Vans, The North Face and Timberland

- Emerging: All other brands. (Altra, Icebreaker, Smartwool, Eagle Creek, Eastpak, Jansport, Kipling, Napapijri, Dickies.)

“As we work to become a more integrated brand-building company, we must operate differently and manage our core and emerging brands in differentiated ways in order to help each of them achieve their full potential.”

That leaves a lot of room as to what it means for the ‘Core’ brands, as much as for the ‘Emerging’ brands. Exciting.

About half-year numbers.

First, let’s remember that Q1 had resulted in what Steve Rendle called VF’s “Fortress Balance Sheet”. Revenue was down 48% and, between other actions, they used leverage to improve liquidity, issuing senior unsecured notes for approximately $2.98 billion.

Well, efforts are paying off.

“Our year-to-date results have surpassed our internal expectations across all brands, driven by digital and China, two of our key growth pillars,”

- Revenue from continuing operations decreased 18% to $2.6 billion,

- Active segment revenue decreased 15%, including a 10 percent decrease in Vans brand revenue,

- Outdoor segment revenue decreased 24%, including a 25% decrease in The North Face brand revenue,

- International revenue decreased 15%:

- Europe revenue decreased 16%

- Greater China revenue increased 16%, including an increase of 21% in Mainland China

- Direct-to-Consumer revenue decreased 17%; but Direct-to-Consumer Digital revenue increased 44%

Digging into the EMEA revenue numbers, we can interestingly see bright spots in our region:

- Vans stopped the bleeding with a 0% revenue change in Q2, from -19% in Q1. Good.

- The North Face is still in a difficult revenue situation, but on an improving trend -15%, vs -21% in Q1.

EMEA numbers are not as good as China, but overperforming the Americas:

With two quarters in the books, VF updated its full year forecast:

- Full year fiscal 2021 revenue expected to be at least $9.0 billion, reflecting a decrease of approximately 14% including a low single-digit growth in the second half driven by a return to growth in the fourth quarter

- Full year fiscal 2021 adjusted earnings per share (EPS) is expected to be at least $1.20, reflecting a decrease of approximately 55%

- Quarterly dividend increased by 2% to $0.49 per share, marking VF’s 48th consecutive year of dividend increases.

VF forecasting its FY2021 EPS landing at $1.20 and revenue at “at least” $9.0 billion shows confidence, beating market consensus of $1.12 EPS and $8.88 billion revenue.

What COVID made clear is that digital capacity is a pivotal asset and solution to many challenges. Not all challenges, but many. Those like VF who invested in time could rely on their digital DTC business to offset stores closure and accelerate their consumer relationship transformation.

Steve Rendle: “Although uncertainties remain, investments in our digital transformation are resulting in near-term momentum and improved capabilities to emerge in an even stronger position”

VF provided better than expected Q2 results and annual forecast, while realigning its brand segmentation. The market is still in a difficult moment – especially with a second COVID wave hitting Europe – but it looks like VF is doing the right thing to go through the crisis and exit stronger than before. Exciting.

Looking forward to seeing Q3 and that Q4 return to growth.