JD Powers Ahead For 1st Half 2021

JD Group Highlights

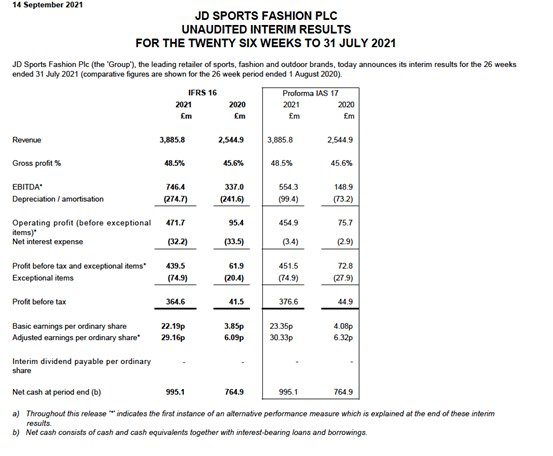

- Record result for the first half with profit before tax and exceptional items of £439.5 million (2020: £61.9 million; 2019: £158.6 million) including significant contributions from United States where the aggregate profit before tax and exceptional items increased to £245.0 million (2020: £73.4 million; 2019: £35.7 million)

- JD business in the core UK and Republic of Ireland market where the profit before tax and exceptional items increased to £170.8 million (2020: £52.0 million; 2019: £114.9 million) with a strong retention of sales through digital channels in the first quarter whilst the stores were temporarily closed, combined with strong pent-up demand after reopening

- Significant acquisitions in the period include: DTLR which enhances the Group’s exposure to key consumer demographics in the highly important East Coast market in the United States, Marketing Investment Group in Poland to give the Group a presence in Eastern Europe for the first time

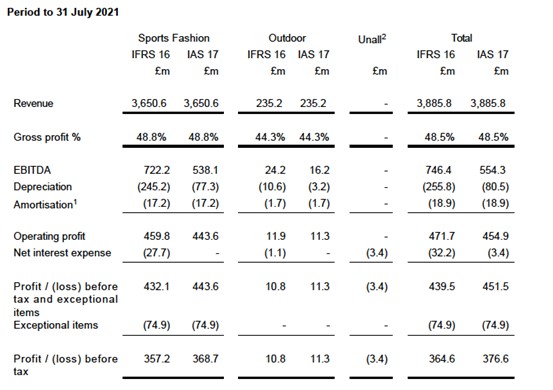

- Outdoor returned to profitability delivering a profit before tax and exceptional items of £10.8 million (2020: loss of £16.8 million)

- Two new major facilities: Derby (UK): 515,000 sq ft facility which will be dedicated to the fulfilment of online orders for JD in the UK with initial go live anticipated by Autumn 2022 and full operational use in early 2023 and Heerlen (the Netherlands): 620,000 sq ft facility which will process substantially all of the volume required for stores and online orders in Western Europe with initial go live anticipated by Autumn 2023 and full operational use by mid-2024

- Forecast outturn headline profit before tax for the full year of at least £750 million

Peter Cowgill, Executive Chairman, said:

“It is most reassuring that the core JD business in the UK and Republic of Ireland performed strongly in the first half delivering a profit before tax and exceptional items of £170.8 million (2020: £52.0 million; 2019: £114.9 million). This result also includes a particularly strong performance from the Group’s banners in the United States which have delivered a combined profit before tax and exceptional items of £245.0 million (2020: £73.4 million; 2019: £35.7 million).”

Significant M&A Transactions

The Group has either completed or exchanged contracts on a number of acquisitions and other investments in the period, which look to either expand the geographical reach of its core premium sports fashion operations or widen the category offer to include other products which are relevant to a style conscious consumer. 80s Casual Classics Limited (’80s Casual Classics’) The acquisition of 80s Casual Classics completed on 2 March 2021 with an initial 70% holding acquired for cash consideration of £14.9 million. Founded in 1993, 80s Casual Classics is an online retailer of heritage and original clothing inspired by the British subculture of the 70s, 80s and 90s. It offers a unique product mix and experience to consumers who look on the much loved classics and genres from the past decades including Indie, Manchester, Rave and various other dance cultures with fond nostalgia. 80s Casual Classics work closely with customers and brands in the relaunch of classic lines collaborating with Ellesse, Fila, Sergio Tacchini and other brands in supplying quality heritage releases and fresh releases based on past styling.

DTLR Villa LLC (‘DTLR’)

The acquisition of 100% of DTLR completed on 17 March 2021 for cash consideration of $504.4 million. At completion, DTLR, which is based in Baltimore, Maryland, had 247 stores trading primarily as DTLR across 19 states principally in urban areas across the North and East of the United States. DTLR has the support of the international brands to expand its store base further in these markets.

It is our current intention to maintain JD / Finish Line, Shoe Palace and DTLR as separate fascias as there is little crossover in locations and they all have their own unique DNA which comes from their retail style and the rich connection with their consumer base. There may, however, be opportunities to enhance our collective operational effectiveness and further enhance the consumer experience in the United States by operating collaboratively in certain areas. Accordingly, DTLR has now been transferred to the same sub-group as Finish Line, JD and Shoe Palace. It was always JD’s intention for DTLR to be part of this sub-group but the requirement for speed and certainty of execution on the original transaction meant that it was more appropriate for the Group to initially acquire DTLR directly.

Marketing Investment Group S.A. (‘MIG’)

The acquisition of MIG completed on 30 April 2021 with an initial 60% holding acquired for total consideration of 344.7 million Polish Zloty (‘PLN’) of which 8.5 million PLN has been deferred subject to customary closing conditions and is expected to be paid in 2022. At completion, MIG, which is based in Krakow, Poland, had 410 stores trading principally as either Sizeer, which is a premium multi-branded fascia not too dissimilar to JD, or 50 Style, which is a multi-branded volume retail concept with lower price points. Whilst the majority of the stores are located in Poland, the Company has also been expanding its reach beyond Poland in recent years and now has stores in a total of nine countries across Central and Eastern Europe. Since completion, Sizeer has further expanded its store base with additional new stores in Bulgaria and Romania. This acquisition also provides the Group with an infrastructure and management team for the development of JD in Central and Eastern Europe with the first store in Poland currently expected to open in the first half of next year.

Deporvillage SL (‘Deporvillage’)

On 25 June 2021, Iberian Sports Retail Group SL (‘ISRG’), the Group’s existing intermediate holding company in Spain, exchanged contracts on the conditional acquisition of Deporvillage which is based in Manresa, Catalonia. ISRG is a leading operator in the sporting goods market across Iberia through its Sprinter and Sport Zone facias with the acquisition of Deporvillage giving additional depth and expertise in the key categories of cycling, running and outdoor. The transaction was subject to certain conditions, principally relating to anti-trust clearance, with formal completion taking place on 3 August 2021. Total maximum cash consideration for the acquisition of an initial 80% holding is €140.4 million of which €40.4 million has been deferred and will be paid contingent on achieving certain future performance criteria.

Update on Footasylum

The Competition and Markets Authority (‘CMA’) announced in its Provisional Report on 2 September 2021 that it was again minded to prohibit the Group’s acquisition of Footasylum. We are very disappointed by this decision as we firmly believed that we had provided compelling evidence to the CMA in its re-examination of the transaction of how the COVID-19 pandemic has materially changed the market for the retailing of international sports brands. In particular, the Group demonstrated very clearly to the CMA how, by causing a structural shift in favour of online shopping, COVID-19 has empowered and accelerated the Direct to Consumer strategies of the international brands as evidenced in their recent public statements. The Group finds it surprising that these key facts have changed so substantially but the CMA’s provisional conclusion has not. In particular, the Group does not understand how the CMA can now acknowledge that JD has no incentive to deteriorate the price, quality, range and service offered at JD after the merger, but then still find that JD would find it commercially rational to worsen the Footasylum retail offer, given that both consumers and brand proprietors expect retailers of premium brands to maintain high standards in retail execution and consumer engagement. The CMA’s findings are, however, provisional and JD remains committed to its transaction goal of improving Footasylum’s resources, access to product and differentiated customer proposition. JD will continue to make its case strongly to the CMA before it releases its Final Report, due in October 2021.

Sports Fashion UK and Republic of Ireland

There was robust consumer demand in our core UK and Republic of Ireland market throughout the period. During the closure period in the Spring approximately 90% of the combined store and online revenues from 2019, which was the last time we traded free from restrictions, were retained through solely digital channels. This represented an improvement on the prior year when the sales retention relative to 2019 was approximately 70% and is a reflection of the enhanced flexibility that we have built into our operational infrastructure in the last year.

There was some pent-up demand when the stores reopened with footfall initially broadly at 2019 levels. However, with conversion significantly ahead of 2019, this resulted in an exceptional like for like growth in stores through April and May, when measured against 2019, of more than 30%. These footfall levels were relatively short lived though with traffic into stores over June and July typically 20% lower than 2019. However, the higher levels of conversion have remained and so, consequently, the stores have continued to trade positively over the last two months of the period with like for like growth relative to 2019 of more than 5%. Revenues through digital channels remain at elevated levels as compared to the period prior to the pandemic with sales in the trading websites representing approximately 30% of total sales since the stores reopened. Prior to the pandemic, sales through digital channels represented approximately 22% of total sales and there is no reason to expect that they will drop back to these historic levels.

We continue to take opportunities to invest in our retail estate where it will further enhance our consumer proposition with a net increase of five stores in the period, which included a store in the new St James Quarter in Edinburgh.

Premium Fashion

As with the core JD fascia, there was a high level of sales retention in the period whilst the stores were temporarily closed. Measured against 2019,around 85% of sales were retained in this period through digital channels, which was approximately 20% higher than thefirst closure period in Spring 2020. Since reopening, the trends have been broadly similar to those in JD with significant initial pent-up demand driving like for like growth in stores through April and May of more than 15% compared to 2019. Again, as with JD, the performance slowed in the last two months of the period with lower footfall through the Summer although higher conversion has ensured that trade in stores is in line with previous levels.

The COVID-19 pandemic and the loss of tariff free, frictionless trade with the European Union have combined to create a challenging operational environment. The most significant disruption was seen in the principal Northern Europe markets of France, Germany and the Netherlands where stores were forced to close fully for a number of weeks. Elsewhere, there was not the same outright closure period in our principal Southern Europe markets of Spain and Italy with trading restrictions implemented on a regional basis. However, when the stores in these markets were permitted to operate, the levels of footfall were significantly lower than pre-pandemic levels with restrictions on customer capacity and trading hours. All markets are currently trading normally with the last market to reopen being Germany where the stores did not reopen fully until mid-June. We are particularly encouraged by the initial performance after reopening in France, Italy and the Netherlands where stronger conversion has offset lower footfall resulting in like for like growth in stores, compared to 2019, of more than 10%. More recently, the performance in Iberia has also begun to stepup consistent with the progressive re-emergence of tourism across Spain and Portugal.

In those Northern Europe markets which suffered full closures, the average retention of sales solely through digital channels in the closure period was around 80% (2020: 60%) with overall growth in digital sales across Europe for the period, when compared to 2019, of more than 150%. Whilst the Group is actively engaged in a number of projects to expand its European logistics infrastructure, online orders in the period were largely fulfilled from the Group’s principal Kingsway warehouse with incremental costs of around £20 million arising from the additional administration and duty costs that now exist consequent to the UK’s new trading arrangements with the European Union. From a longer term perspective though, it is encouraging that there is a broadening base of consumers in Europe who are comfortable engaging with JD through any channel. The current operational challenges are very much temporary in nature and we retain our belief in the long term opportunity across Europe. Accordingly, we remain committed to expanding our physical retail presence in Europe with a headline target of opening one store per week on average. Restrictions placed on construction activity in a number of markets constrained the number of stores that we were able to open during the first half, although we have opened 14 net new stores to date.

Sprinter & Sport Zone

As with JD, our Sprinter stores in Spain were largely able to remain open throughout the period although, periodically, there were restrictions placed on them in terms of trading hours or customer capacity. There was a strong performance in key active sports categories with COVID-19 proving to be a catalyst for many consumers to increase their participation in sports and fitness.

The Sport Zone stores in Portugal were closed in the first quarter and reopened in May. The improvement in performance of the business under the Sprinter management team has continued in the period.

Outdoor

Our Outdoor businesses have had a much improved first half capitalising on the current strong demand for outdoor living and cycling categories, with an elevated demand currently for holidays in the UK combined with a general recognition of the physical and mental health benefits that come from spending time outdoors. Whilst we are encouraged by our performance in the period, we do recognise that the current popularity of domestic holidays may be temporary although, by no means did our businesses achieve their full potential in the period, with supply chain delays negatively impacting the performance of certain seasonal categories combined with insufficient global production capacity to meet current strong demand for bikes and cycling related accessories. Elsewhere our program of works to enhance the profile of certain categories such as fishing and equestrian has gained momentum with the opening of 16 additional Fishing Republic concessions in key locations combined with the opening of the first Naylors equestrian concession in Kidderminster.

Supply Chain Developments & Brexit

UK

The warehouse at Kingsway, Rochdale has been the Group’s primary facility for the UK and Europe since 2012 and, even allowing for a program of continual investments, some of the original equipment, which was largely focused on the picking of product for stores, will start to approach the end of its natural useful life over the next few years. A program of works to update this equipment would require sections of the facility to be effectively decommissioned for periods of time. However, as sales from online channels are likely to remain at the current elevated levels and the processing of large quantities of small volume orders for online is very space intensive, we have concluded that there is insufficient spare capacity at the site, particularly at peak periods, to accommodate an upgrade programme without risking service levels. We are also mindful that the activity in our warehouses may be constrained for some time yet through the requirement to operate with some form of social distancing. consequently, the Group has concluded that it needs additional warehousing capacity in the UK which can be dedicated to the fulfilment of online orders. In the short term, this additional capacity will be provided by Clipper Logistics Plc who are providing a range of logistics operations, including warehousing and e-fulfilment. This is presently considered to be a temporary solution though and the Group has now exchanged contracts on a long term lease on a new 515,000 sq ft facility in Derby which will be used exclusively to fulfil online orders in the UK. This facility, which is being constructed to the latest environmental standards including rainwater harvesting and electric vehicle (EV) charging infrastructure, is scheduled to be handed over for fitting out later this year. Detailed selection programs for warehouse management systems and specialist automation equipment for processing large volumes of online orders are underway with initial go live anticipated for the site by Autumn 2022 although it will be early 2023 before the site is fully operational. We would currently estimate capital investment of approximately £70 million on the new site in Derby over the next two years to deliver this initial program of works of which approximately £35 million is expected to be incurred in this financial year. The Kingsway facility will then largely focus on the provision of product to the JD stores in the UK although it will also have spare capacity to fulfil online orders for the JD fascia in the UK at peak periods.

Western Europe (including the Republic of Ireland)

The terms of the UK’s trading agreement with the European Union mean that we no longer enjoy tariff free frictionless trading with our former European partners. As a consequence, we are now incurring some duties on the transfer of goods from the UK into EU countries. There is also a significantly enhanced administrative burden and whilst our operational systems have been configured to sort stocks as required by the Customs Authorities and to produce the necessary documentation in the right format, this does not guarantee that goods flow freely into the EU, with an unexpectedly high proportion of trailers stopped at the border for detailed manual checking. This can add several days on to delivery timelines but, until a particular trailer is pulled for inspection, we do not know which specific deliveries will be impacted. We have been able to reduce our exposure to the adverse consequences of Brexit through our 80,000 sqft third party warehouse in Southern Belgium which opened in Autumn 2020 and is functioning very effectively. This site is already receiving stocks and fulfilling a large proportion of the core ranges and fastest moving lines required for stores in Mainland Europe. However, it does not provide a solution for online orders. Therefore, to complement this facility in Southern Belgium, we have now signed a short term lease on a 115,000 sq ft facility which is located in Lille, Northern France which will be dedicated to processing online orders for a number of countries across Mainland Europe. The fit out of this site and installation of Group systems has now commenced with customer orders beginning to be fulfilled from this site ahead of the peak trading period. As our business in Western Europe increases in scale and complexity, we are looking to build a cost effective, service orientated supply network which can support business growth both in stores and online Elsewhere, our new 65,000 sqft warehouse near Dublin will begin receiving stock from suppliers shortly which will facilitate the supply of product to stores and fulfilment of online orders in the Republic of Ireland ahead of the peak trading period.