Pro Content

Pro Content

Globe International Ltd Release FY23 Financial Results, Ended June 2023

Globe International Ltd reported an improvement in performance in the second half of the year. Compared to the first half of the financial year, profitability was higher despite sales being lower, as the clearance of excess hardgoods inventories began to wind down and other positive business changes began to take effect.

The key business metrics for the year were as follows:

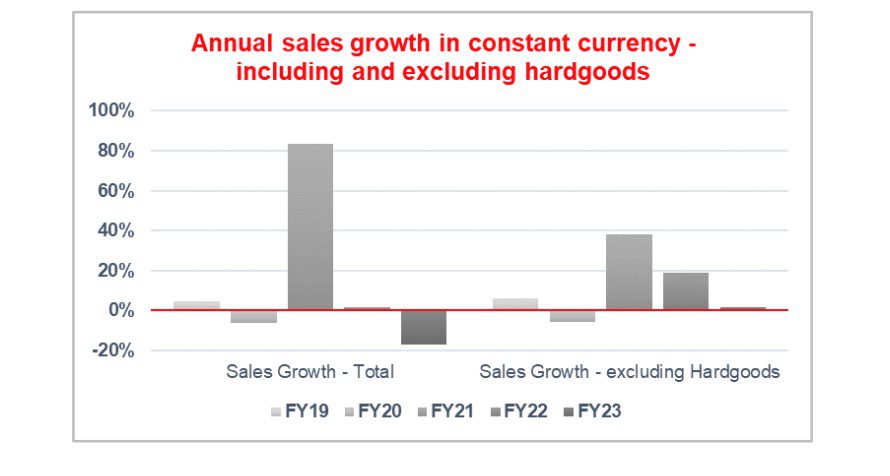

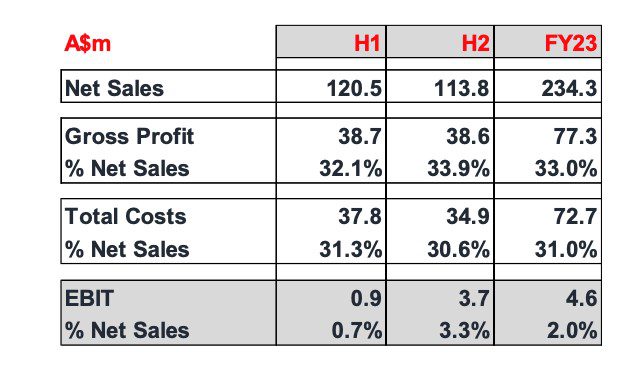

- Reported annual net sales of $234.3 million declined by 15% compared to the prior year.

- Excluding all hardgoods sales, net sales grew by 2% in constant currency terms.

- Earnings before interest and tax (EBIT) were $4.6 million. EBIT in H2 was $3.7 million, compared to $0.9 million in H1. Underlying EBIT for the year was $12.5 million.

- Net profit after tax (NPAT) was $1.6 million.

- Cash-flows provided by operating activities were $12.1 million, fuelled by lower hardgoods inventories.

Matt Hill said, “The downturn in the hardgoods market from the second quarter of FY22 had a significant impact on FY23 financial performance, compared to the prior two years when hardgoods generated massive sales and profit growth. In addition, there were multiple factors that put downward pressure on gross profit margins. This included exceptional clearance sales due to excess hardgoods inventories that built up as a result of logistics delays and the market downturn which resulted in an industry wide inventory glut, as well as the strength of the USD, and heightened freight costs.

However, we moved quickly to address these issues, while our apparel brands remained stable. Consequently, profitability improved in the second half of the financial year, and we ended the financial year in a much stronger financial position. Cash generated from operations was $12.1 million, helping to reduce our reliance on banks for working capital funding by 77%, with just $3.2m in facilities utilized at 30 June 2023. With improving margins, right-sized inventories and a stabilization in sales from our strong apparel brands and with a low base of hardgoods sales, we are in a good position as we head into FY24 to see profitability improve.”

Net sales of $234.3 million were 17% lower than the previous financial year due to the reduction in hardgoods sales. The $4.6 million EBIT reported for the year generated a return of 2.0% on net sales, compared to 10.0% in the previous corresponding year. The decline in profitability was caused by the reduction in hardgoods sales, the strength of the USD, excessive clearance activity, restructuring costs and inflationary pressures on costs across the business.

On a regional basis, the Australian Division continued to be the most stable and profitable of the 3 regions, while the US was most heavily impacted by the clearance of excess hardgoods inventories, which are non-recurring. The European business generated an operating loss for the financial year. The loss was caused by a combination of macro factors and internal management issues.

Extensive restructuring has occurred over the second half of the year, including replacing the management team, and performance is expected to improve in FY24 and beyond. As a result of changes made throughout the 2022 calendar year to address the collective issues that negatively impacted profitability, gross profit margins were higher and costs were lower in the second half of the year, resulting in an overall increase in profitability, Matt Hill said. It can be seen that underlying margins are healthier in the go-forward business, and that revenues and margins are higher than they were pre-pandemic.

In short, the hardgoods boom drove exceptional profits and shareholder returns in FY21 and FY22, but the downturn negatively impacted profitability in FY23. If we strip away the impact caused by the hardgoods cycle, there is an underlying apparel business that has grown over the last 4 years. Now, as we emerge on the other side of the pandemic-related boom, we have a larger, more stable company than we did pre-pandemic, with global apparel brands of much larger scale, operating in diverse distribution channels around the world.”

The Group’s cash position, net of working capital borrowings, was $7.8 million at 30 June 2023, significantly higher than the low-point at the end of the first quarter of the financial year. The $12.1 million in cash that was generated from operations over the financial year was returned to shareholders via dividends ($7.5 million) and used in investing ($1.7 million) and other financing activities ($2.3 million). The cash from operations was bolstered by a $6.3 million reduction in working capital over the year, driven by the $18.5 million reduction in inventories, with an associated partial reduction in trade payables. The working capital position at the end of the financial year is more reflective of the on-going working capital needs of the business. The capital expenditure incurred during the year included the completion of the refurbishment of the Melbourne-based company-owned retail and distribution facility acquired in the prior year. Going forward, capital expenditure is expected to return to normalized levels of $0.5 – $1.0 million.

In review, Matt Hill said, “The last twelve months have been challenging but I am proud of how fast our team has moved to rectify the situation. We have restructured where needed, cleared inventory as required, and made adjustments to both pricing and the cost base. Consequently, we enter FY24 with these restructuring efforts largely completed, and now look to improve profitability in FY24 with a stable base of revenue and strong margins from our apparel and footwear brands, and a right-sized hardgoods business.

We continue our evolution as a branded apparel, footwear and hardgoods company and now have an excellent platform of key apparel and footwear brands in FXD, Salty Crew and It’s Now Cool to drive reliable future growth globally, while maintaining our core heritage in hardgoods with the Impala and Globe brands. Of course, our business relies on consumer discretionary spending, so to the extent that inflation and interest rates impact the availability of discretionary spending over the next 12 months, the sales outlook is uncertain. Current retail feedback certainly suggests that the market is tough.

However, while it’s very early in the year, the positive trends we saw in the latter part of FY23 seem to have continued into the start of FY24, with sales in July stabilizing and profits higher than at the same time last year. Looking ahead, at this stage it is too early in the year to give any reliable sales outlooks.

But, as things stand today, we expect profitability to improve based on a lower cost base and higher gross profit margins, compared to FY23, and for revenues to stabilize. Further updates will be provided at the Annual General Meeting in October, after the first quarter of FY24 has been completed.”